Last updated date: February 9, 2026 | 11:19 pm

Table of Contents

![]() Editor's Note: This

article reflects current invoicing rules and compliance guidance as

of 2026.

Editor's Note: This

article reflects current invoicing rules and compliance guidance as

of 2026.

Many business owners in the Philippines are still confused about whether to issue a Sales Invoice or an Official Receipt, especially after the changes introduced under the Ease of Paying Taxes (EOPT) Act. This confusion is common among service providers, small businesses, and growing companies trying to stay compliant with BIR requirements.

Since the EOPT regulations were released in April 2024, the focus has shifted from

understanding the change to proper implementation and compliance.

This guide explains the difference between a Sales Invoice and an Official Receipt, when to

issue each, and what businesses need to do today to stay compliant.

What is the EOPT Act?

The Ease of Paying Taxes (EOPT) Act,

signed on January 5, 2024, modernizes and simplifies

tax administration in the Philippines, making it more taxpayer-friendly.

This regulation outlines amendments to our tax system,

including the reclassification of

businesses, easier tax return filing, and simplified value-added tax (VAT) rulings.

Watch this to learn more about the EOPT Law and other recent tax changes in the country:

In addition, the EOPT Act involves significant changes to the invoicing requirements,

pushing businesses to now use invoices instead of official receipts (ORs).

The Bureau of Internal Revenue (BIR) also released the following memoranda—RR 7-2024 and

RR 11-2024—to provide more

clarification on this transition.

What are the differences between an official receipt and an invoice?

Before the EOPT Act took effect on April 27, 2024, companies could use official receipts or

invoices depending on the nature of their business.

Businesses selling goods and properties use invoices as their primary documents, while those

selling services or leasing properties use official receipts.

However, the EOPT Act has amended the use of these documents.

Here are the key differences between official receipts and invoices:

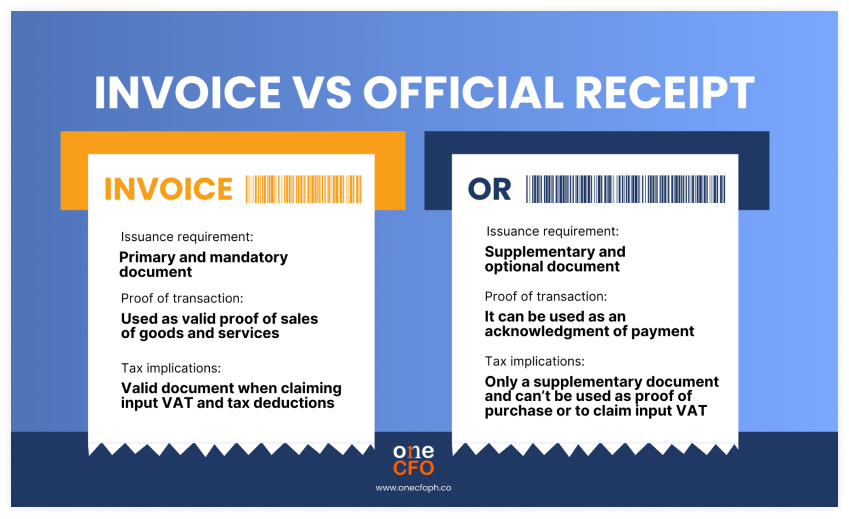

Issuance requirement

According to the EOPT Act, businesses should now issue invoices as the primary document for

selling goods and services.

Also, it’s worth noting that an invoice doesn’t just refer to a sales invoice. Businesses

can add any descriptive name to label their invoices, such as “Cash Invoice,” “Credit

Invoice,” “Service Invoice,” “Billing Invoice,” and more.

On the other hand, official receipts are only secondary and optional. If your business still

decides to use ORs, you must register them to the BIR as a supplementary document to get a

new Authority to Print (ATP).

Proof of transaction

Under the EOPT Act, businesses must use invoices as proof of their sales, regardless of

whether customers pay in cash or on credit. If the customer pays in credit, meaning the

business collects the payment later, business owners should not issue a second invoice upon

collection.

Instead, businesses can issue an official receipt as proof or acknowledgment of payment once

the customer settles their outstanding balance.

Tax implications

If you want to take advantage of tax-deductible expenses, remember

that invoices are

considered valid documents for tax deductions.

Moreover, VAT-registered businesses can now use the invoices they receive as input VAT when

buying from other VAT-registered companies.

Meanwhile, official receipts are no longer valid when claiming a tax-deductible expense or

input VAT.

Frequently Asked Questions About EOPT Invoicing Changes

Since the release of the EOPT Act, many businesses are still adjusting to the new invoicing rules. To help clarify what applies today, this section addresses the most common questions about Sales Invoices, Official Receipts, and proper invoicing compliance.

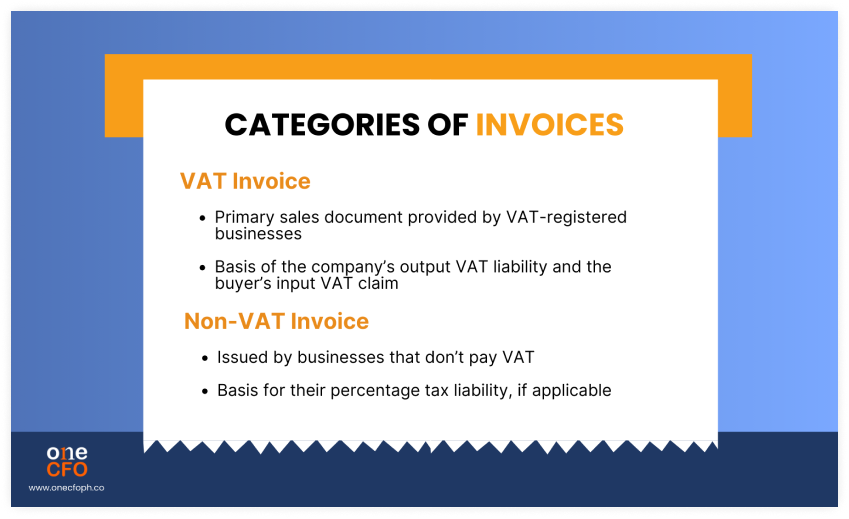

What are the two categories of invoices?

Invoices are categorized based on VAT status: VAT invoices for taxable sales and Non-VAT

invoices for exempt or non-VAT transactions. Each must show the correct breakdown of

VATable, zero-rated, and exempt sales.

The BIR defines an invoice as a written account

evidencing the sales of goods and services

issued to customers. There are also two categories of invoices as follows:

If you’re a VAT-registered business selling zero-rated or VAT-exempt products, note that you

can use a single invoice for mixed transactions, including goods/services subject to VAT,

Zero-rate, and VAT-exempt sales.

When doing so, it’s essential to show a breakdown of the amounts for each type of sale:

VATable sales, VAT amount, VAT-exempt sales, and zero-rated sales.

When should you issue an invoice?

VAT-registered businesses must issue an invoice for every sale, regardless of amount.

Non-VAT businesses must issue an invoice when the sale exceeds ₱500, the buyer requests it,

or total daily sales under ₱500 exceed ₱500.

The timing of when to issue an invoice depends on whether you’re VAT-registered and the

amount involved in the transaction.

VAT-registered sellers should always invoice all sales transactions, regardless of the

amount.

Meanwhile, non-VAT-registered businesses must issue an invoice when they meet at least one

of these three conditions:

Also, note that the BIR will adjust the ₱500 threshold every three years based on the Consumer Price Index.

What happens to your existing official receipts?

Unused Official Receipts can still be used as supplementary proof of payment, or they can be

converted into invoices by striking out “Official Receipt” and stamping “Invoice.”

If you still have unused booklets of official receipts in your hand, don’t throw them away!

Even though invoices are now the primary document, you still have two options for utilizing

your unused receipts until they’re fully consumed.

The first option is to use your remaining receipts as supplementary documents for your

business. If you still issue an invoice for the same transaction, you can issue a receipt to

acknowledge your customer’s payment.

If opting for the first option, stamp the OR with the words “THIS DOCUMENT IS NOT VALID FOR

CLAIM OF INPUT TAX.” Doing so reminds buyers that they can’t use ORs to claim input tax.

The second option is to convert unused receipts into invoices, which is very beneficial for

businesses that have yet to print their invoices.

To do this, just strike out the words “Official Receipt” in your OR and stamp it with

“Invoice,” “Sales Invoice,” “Cash Invoice,” or any other variation that includes the word

“Invoice”.

Additionally, you must report the inventory of unused receipts to the BIR to be converted to

invoices.

What about businesses using cash registers or POS machines?

Businesses with CRM or POS systems can replace “Official Receipt” with “Invoice” in their

system without prior BIR approval, but must report the starting invoice serial number to the

BIR.

If your business uses cash register machines (CRM) and point-of-sale (POS) machines, you can

simply replace “Official Receipt” with “Invoice” in your systems without notifying the BIR.

However, these businesses must still submit a notice to the BIR specifying the invoice’s

starting serial number, which should follow the serial number of the last issued OR.

Are online sellers affected by the invoicing regulations?

Yes. Online sellers using e-receipting or e-invoicing software must issue invoices instead

of traditional receipts and report their starting serial number to the BIR.

Similar to the new withholding tax rule, the recent

changes in invoicing regulations are

also applicable to online sellers.

Although online sellers don’t use CRM or POS, they typically rely on e-receipting or

e-invoicing software to issue their sales documentation. Like businesses using CRM and POS,

online sellers can replace “Official Receipt” with “Invoice” in their software.

Additionally, they must report to the BIR the starting serial number of their invoice,

following the same procedure as those with CRM and POS.

What about businesses using computerized accounting or books?

Businesses using computerized accounting systems or computerized books of account must

ensure their system configuration complies with current BIR invoicing rules and that any

system changes are covered by an approved CAS or CBA application.

If your business uses a computerized accounting system (CAS) or computerized books of account (CBA),

you should reconfigure your systems and file for a new application to use CAS

or CBA.

Filing a new application involves surrendering your current Acknowledgement Certificate (AC)

or Permit to Use (PTU) and applying for a new one.

The BIR previously required affected businesses to complete CAS or CBA updates by December

31, 2024. While this transition period has passed, businesses that updated or modified their

systems must ensure their CAS or CBA is properly reconfigured and covered by an approved BIR

application.

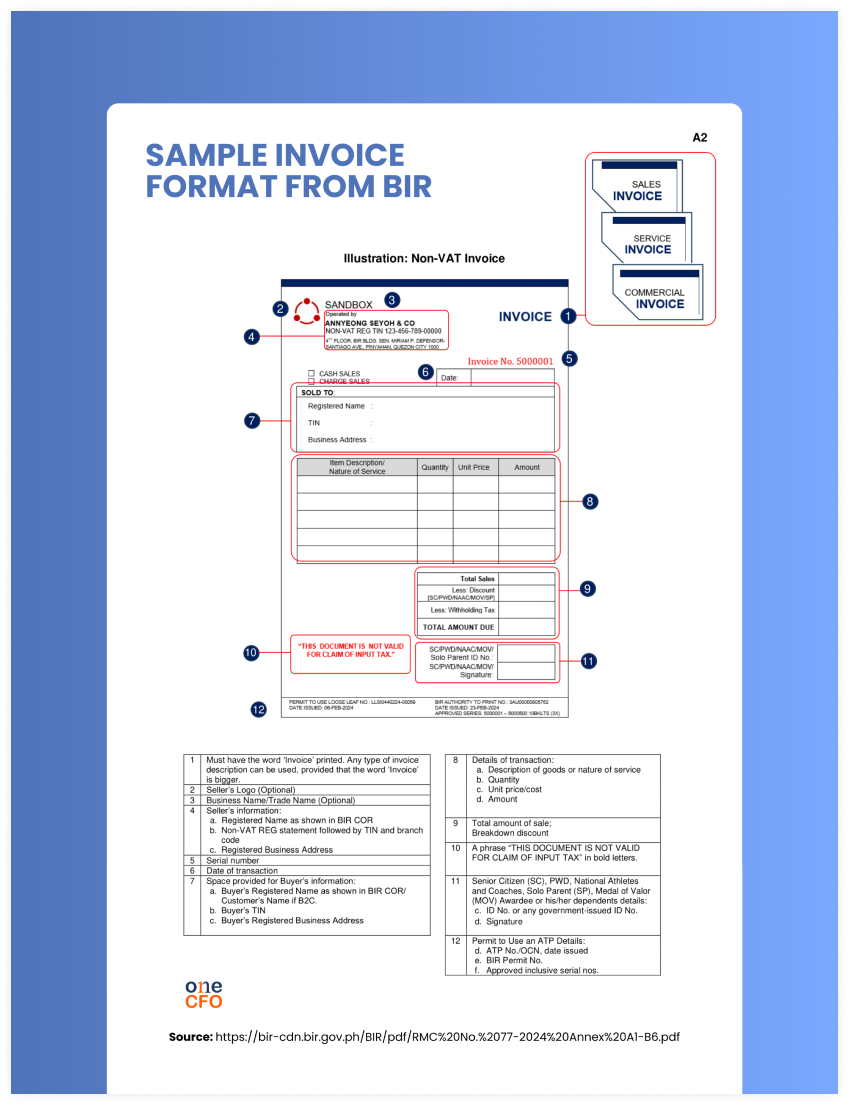

What should be the format of an invoice?

A compliant invoice must include the seller’s TIN, registered business name and address,

invoice label and serial number, buyer details, itemized goods/services, VAT breakdown (if

applicable), and total amount.

Now that invoices are the primary document for proof of sales, businesses should secure an

Authority To Print (ATP) from the BIR before going to an Accredited Printer to print their

invoices.

Here are the following information to include in your invoice format:

What are the consequences of non-compliance?

Failing to issue the proper invoices, using ORs as primary proof of sale, or incorrect

documentation can lead to fines (₱1,000–₱50,000) and even possible imprisonment under BIR

rules.

Non-compliance with the new invoicing regulations set by the EOPT Act, such as non-issuance

of invoices, failing to stamp an OR, and the like, is subject to a penalty of ₱1,000 to

₱50,000.

In addition, non-compliant business owners may be imprisoned for two to four years.

Are there any e-invoicing updates businesses should know about in 2026?

Yes. While the core invoicing rules introduced in 2024 remain in effect, the major focus in

2026 is on electronic invoicing (e-invoicing)

compliance and proper implementation.

In 2026, businesses are expected to move beyond understanding the invoicing rules and focus

on how invoices are issued, recorded, and transmitted.

Selected taxpayers, particularly e-commerce sellers, large taxpayers, and businesses using

computerized accounting systems, are required to comply with BIR e-invoicing requirements,

with deadlines extending through December 31, 2026.

At the same time, businesses must ensure that all invoices, whether electronic or manual,

contain the mandatory information and fields required by the BIR.

Using Official Receipts as primary sales documents, issuing incomplete invoices, or failing

to comply with e-invoicing requirements can still result in fines or legal penalties.

Still Have Questions About Philippine Tax or Invoicing?

Some tax and invoicing situations don’t fit neatly into FAQs. If you have specific questions

about BIR invoicing rules, e-invoicing, or other Philippine tax matters, you can ask

directly through DocTax or connect with a licensed tax professional.

DocTax lets business owners get reliable, Philippines-specific tax answers without guesswork

— helping you make informed decisions and stay compliant.

👉 Ask a

Philippine tax question through DocTax.

Stay compliant with the new invoicing regulations

Staying compliant with BIR invoicing requirements remains essential for businesses in the

Philippines.

While the core rules under the EOPT Act remain in effect, the focus today is on proper

implementation, accurate documentation, and readiness for electronic invoicing to avoid

penalties and compliance issues.

After understanding the differences between Sales Invoices and Official Receipts, the next

step is to ensure that your invoicing process, systems, and records align with current BIR

requirements.

Sales Invoice vs Official Receipt

Key Takeaways

If you need support navigating invoicing compliance, electronic invoicing readiness, or

broader tax requirements, OneCFO is

here to help. Our team of finance and accounting

professionals provides practical guidance to help businesses stay compliant while

supporting sustainable growth.

Visit us at onecfoph.co or email us at [email protected] to

learn how OneCFO can support your business through ongoing regulatory and tax compliance

changes.

Read our disclaimer here.

About OneCFO

Based in the Philippines, OneCFO provides tech-enabled fractional CFO, bookkeeping, tax management, and payroll

support to startups, scaleups, and small- to mid-sized businesses across Southeast Asia.

We help companies manage cash flow, fundraising, and financial strategy. With our fractional CFO expertise,

business owners and finance teams gain clarity in finance and the confidence to grow.